It’s that time of the year again! As 2020 draws to a close, Malaysians are rushing to maximize their income tax returns. 2020 has not been a great year, with COVID-19 and the subsequent economic challenges. It’s often said that the only two constants in life are death and taxes. I couldn’t think of a better descriptor for 2020. So pull up a chair and order a kopi o kosong kao coz limpeh is going to intro you to a 21%+ guaranteed ROI investment. This is not a scam or money game ah. Conlan79firm good stuff.

What is PRS?

PRS stands for Private Retirement Scheme. It’s EPF’s private cousin. Think of it this way, if EPF is your school canteen, PRS is the corner coffee shop auntie that brings steaming hot bowls of laksa and pan mee to the school gates to sell. They can be a lot more delicious (profitable) than your canteen nasi lemak, if you choose the right dishes (funds).

They’re also 100% legal and above-board coz the corner coffee shop auntie already settle this arrangement with the school principal (Malaysia gahmen).

Why should you invest in PRS?

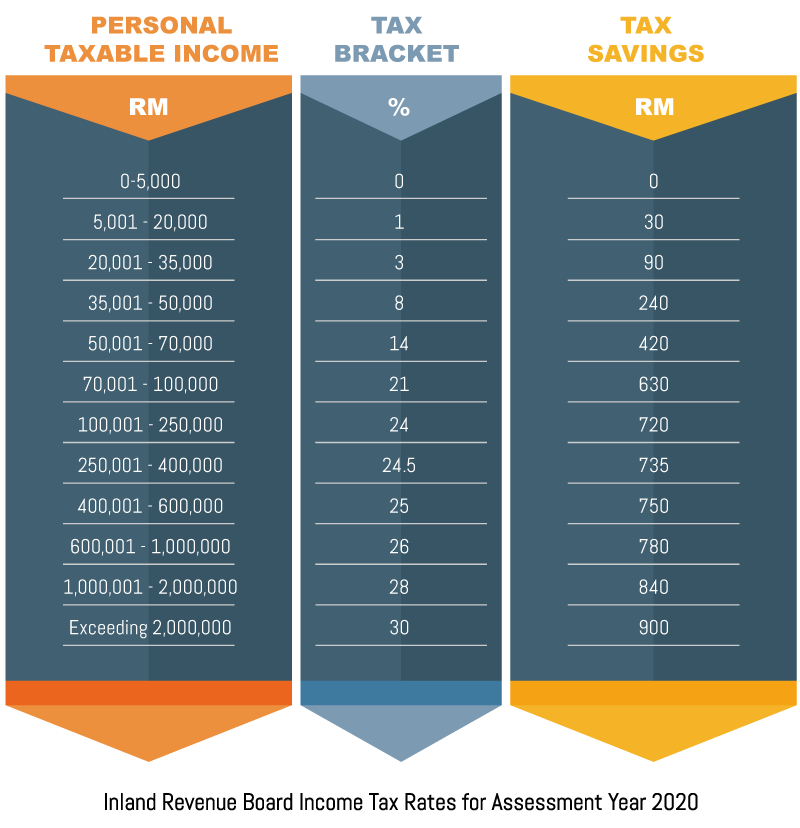

Simple! For the RM3,000 tax benefit! Here’s a simple chart I stole from PPA so you can visualize how much you stand to enjoy from tax deductions:

If you’re earning RM10,000 per month (putting you inside the RM100,001-RM250,000 tax bracket), you’ll get a 24% return of up to RM720. This number increases the more you earn, but inversely also decreases the less you earn.

It’s still worth it if you have money to spare!

Which PRS fund should I invest in?

I did a lot of research back in the days to find the best fund to invest in. Of course, the standard disclaimers apply: Past performance is not indicative of future results, this is not a buy recommendation blah blah blah.

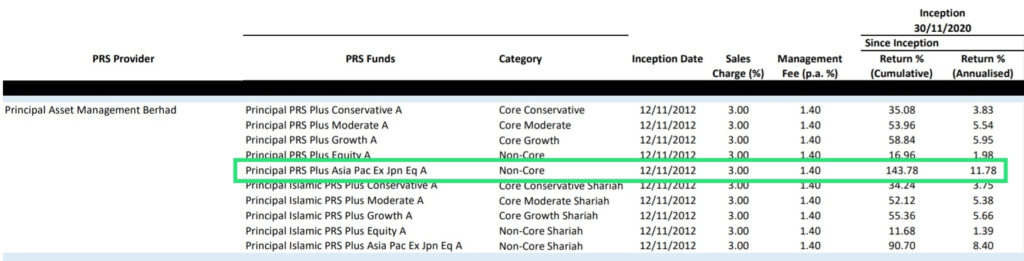

Let’s look at the numbers coz figures, just like hips, don’t lie:

It is clear from the image above that one fund stands head-and-shoulders above the rest with 11.78% annualized returns – Principal PRS Plus Asia Pacific Ex Japan Equity. This performance has been remarkably consistent since inception. If you want to delve deeper into their product factsheet, there was one year (2018) where they did poorly, but they generally exceed their target 8% PA returns except for two years.

This is the only fund I’m invested in. I top-up 3k into Principal’s PRS Plus Asia Pacific Ex Japan Equity every year.

Class A or Class C? What’s the difference?

Class A funds are front-loaded, which means they have a higher sales charge. Class C has lower sales charge but it has a slightly higher management fee.

Principal PRS Plus Asia Pacific Ex Japan Equity – Class A

Sales Charge: 3%

Management Fee: 1.4%

Principal PRS Plus Asia Pacific Ex Japan Equity – Class C

Sales Charge: 0.5%

Management Fee: 1.5%

Napkin math says that in order to “make up” for the extra 2.5% in sales charge for Class A, you will need to be invested for more than 25 years, “saving” 0.1% each year in management fees. Of course, the actual calculations are more complicated that that but for most people, Class C will make more sense as the fees are averaged out each year based on the NAV (Net Asset Value).

I’m writing this coz I wished PRS was explained in an easy-to-understand manner when I first started investing. If you found this content useful, please Like DamnChun on Facebook for more! 👍🏻

Kena some good stuff and invest in PRS before 31st December 2020 to qualify for the tax benefits!

Sign-up for Private Retirement Scheme (PRS) via the official PPA website! PPA is the central administrator for PRS in Malaysia. You can choose the PRS fund you want and invest in it entirely online!